Sometimes, 1 + 1 = 3.

Not mathematically, of course. But sometimes, when you add things together, the sum is far more powerful than its parts.

Over the last 24 months, Stonewood Financial has launched multiple new tax, IUL, and annuity tools that you can use to grow your practice. This blog post aims to show you how to combine them all into one package—making 1 + 1 = 3 for your clients.

Crafting Plans for Your Clients

One of the most common questions I hear from advisors is: I love Stonewood Financial’s tax reports, but how do I put them all together for my clients?

One of the most popular tax reports in our industry is Stonewood Financial’s Total Tax Burden Analysis. It’s also one of the best conversation openers in the business, getting people interested in addressing their tax problems.

But there’s more to addressing taxes than just a report. Advisors want to know: What does the sales process look like? Should you do Roth Conversions with an annuity or use IUL? Most importantly, how do I seamlessly fit it all together for my clients?

Delivering Max Value

For example, let’s use a 60-year-old couple with $2,000,000 in investable assets. This is the potential money in motion for many clients as they approach retirement. And they are talking to you because you are the advisor in your market who can articulate the growing concern over tax risk and put together a complete plan that mitigates market risk, income risk, tax risk, AND legislative risk.

Let's list out some goals for this sample client:

- Retire Comfortably: With a 60-year-old couple, retirement might not be there yet, but it's on the horizon, and people just want to retire comfortably. So, in this example, I'm assuming they want to retire at age 70.

- Be Strategic: These clients want to make good decisions—especially when it comes to taxes. (It must be all that good work you did educating them in your workshops, marketing, and prospecting.) They want to address the tax problem that exists for future retirees who are overly invested in tax-deferred vehicles like IRAs and 401(k)s.

- Legacy: A third goal for this sample couple is to have something left over for the kids. Like many retirees, it doesn't necessarily have to be a large windfall, but a little bit left over for the heirs is often on the list of goals.

- Control: These clients want flexibility to change with the times. Many times, you don't hear this from the customer. In fact, when competitors want to find fault in index products (like annuities or IUL), one of the objections that tends to get thrown out is a lack of control. I believe this is just an illusion, but it’s important to show how this plan will work even if things don’t go exactly as planned.

Putting Together a Blueprint

Here’s how we might help this couple optimize their retirement approach in the tax-free space:

- ACAT the account over to a conservatively managed account portfolio. This allows you to use the entire portfolio to execute a self-contained strategy.

- Open an FIA with a portion of the assets. This locks in a guaranteed income stream to help with the “retire comfortably” goal. Using a carrier that allows Roth conversions within their annuity contracts is important as these assets will be converted to Roth later in the plan.

- Start a 10-year conversion process for the client. The goal of this tax reallocation plan is to have about half of the portfolio available for tax-free income starting at age 70 (the 11th year).

A. Part one of this process is to establish a 5-pay IUL. The IUL will provide a supplemental tax-free retirement income plan while also offering up a tax-free death benefit to the kids. The client will use IRA dollars to both fund the policy and cover the taxes due during the conversion. This will be the first 5 years of the conversion process. One important thing to remember about taxes: Advisors often have tough conversations with clients about “generating” taxes during the conversion. Remember, that’s the point. Clients are paying those taxes when it’s most strategic. Don’t let the fear of more taxes in the present prevent massive tax savings in the future.

B. Part two will begin in year 6 as you begin to convert the FIA assets to Roth. This will be another 5-year plan, with the final conversion happening in year 10 overall. With an income goal of Age 70, this makes the 5-year rule for Roth conversions a non-problem. Make sure you are using a carrier that can administratively allow for Roth conversions within the account. - At the end of the 10-year conversion process, your client should have the following in place:

A. Half of the assets in one of your managed account portfolios. These assets remain tax-deferred. If you are an insurance-only producer, perhaps an accumulation-focused FIA could be suitable.

B. About 25% of the assets will be in a fully funded IUL policy.

C. Another 25% of the assets will be in an FIA that has been fully converted to Roth

Of course, Stonewood Financial has tools to help you with each step of this process.

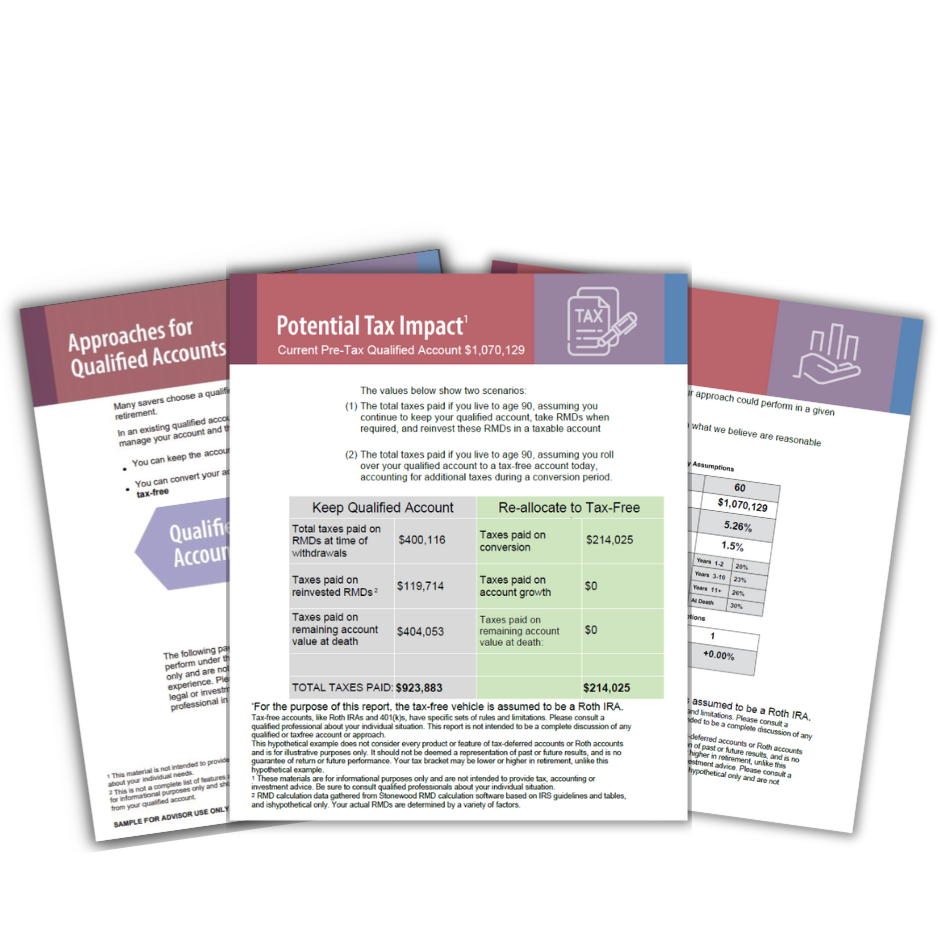

Total Tax Burden Report: This report helps you calculate the total retirement tax bill for the assets earmarked for conversion. This will be the amount going into the FIA and the IUL, plus the amount of tax projected to be paid during the 10-year conversion. It might make sense to allocate additional assets to the conversion to account for tax drift, IRMAA, and the Trump Tax cuts expiring during the conversion. Do not let those potential hiccups disrupt the conversion. Just plan for them in advance to ensure the math works out in the client’s favor. (Spoiler alert: most times the client still comes out way ahead.)

This calculation early in the sales process will help establish the tax problem at hand, validate the need to reallocate a portion of assets to tax-free, and then show a path forward through conversion.

Here’s a sample of what that Total Tax Burden assumptions and analysis look like:

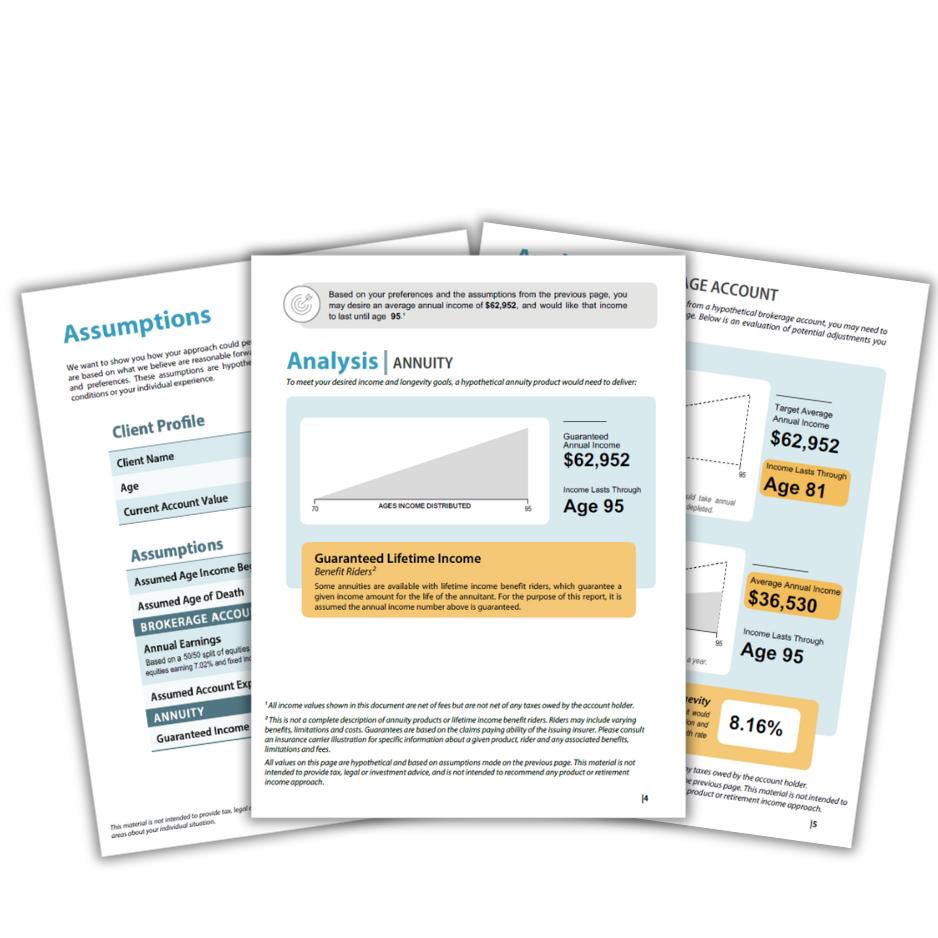

Annuity Alpha: This report is critical to answering the most common question Googled about annuities...” Are annuities a good investment?” Run the carrier annuity illustration, plug the guaranteed income amount into Stonewood Financial’s Annuity Alpha software, and you’ll have a compliant report to use with clients that will tell you what the capital markets would have to deliver to match what the annuity guarantees.

And with that, you’ll have an answer to the question, “Is this a good deal?” (Another spoiler alert: they usually are.)

Tax & Income Reports: These Stonewood Financial reports allow you to compare the potential after-tax income that can be created based on realistic, reasonable assumptions in a variety of approaches - from systematic withdrawal plans from Traditional and Roth IRAs, to illustrated income amounts from annuities and tax-free policy loans from IUL. The output creates a simple report for a quick view analysis of after-tax income from financial instruments.

Putting it All Together

Now let’s add it all up and compare these clients’ options at a 20,000-foot view.

For this comparison, I’m only considering the assets that are earmarked for conversion. I'm assuming that about half of the $2M total remains in the existing strategy. Since we’re comparing, the results for that half of the portfolio would be the same in each option.

The results below focus on the assets used to fund an FIA, IUL, and tax payments to the IRS during conversion. That total comes to just over half of the portfolio ($1.07M to be exact).

Option 1: Let’s look at what the projected results of this couple “doing nothing” would be. Well, that’s not really fair. They did something. They actively chose to continue to defer taxes. That strategy would yield the following projected results:

-

$62,000 per year of after-tax income starting at age 70

-

Assuming the client passes away at age 95, the total after-tax income generated would be $1,856,000

-

This example liquidates the account at age 95, so there are no remaining assets to pass on in the form of a legacy

Option 2: Now let’s consider the projected results of the 10-year conversion plan. That means following the path I outlined earlier in this article:

-

Fund an IUL policy in the form of 5 payments over the plan's first five years

-

Open an FIA at Age 60 and begin that conversion process in years 6-10

Following this path means by age 70, about half of the client’s assets would be available for tax-free retirement income. The combined results would be as follows:

-

The IUL, based on a sample illustration I ran using realistic, reasonable assumptions, could generate about $45,000 annual tax-free loans from the policy

-

The FIA, now converted fully to Roth and including a guaranteed income rider, would generate about $63,000 of tax-free income based on a sample illustration I ran. And yes - those FIA funds are guaranteed.

Add them together and you get an impressive $108,000 income projection. Assuming the client lives to age 95, you would have $2,676,000 of total income. AND there is even a nice $300,000 death benefit for the kids that pushes the total benefit to nearly $3M. All income tax-free.

I want to dive a little deeper into some of the “what ifs”. You might be thinking I set up this example in the best-case scenario. Maybe you are thinking this new plan has an annuity included, which will always benefit the clients that outlive life expectancy. So of course the example that goes well beyond life expectancy is going to win out versus a plan without a guaranteed income element.

And if you said that, I would have no choice but to agree. But here’s the thing...this plan has two key financial instruments. One of those instruments benefits the client if they live a long, healthy life well past life expectancy. That would be the annuity. The other key financial instrument self-completes this approach in the eyes of tragedy. That would be the IUL. If the client passes away early into retirement, a large tax-free death benefit immediately passes to heirs.

The combination of these two instruments is what makes this conversion plan so powerful, whether the client lives a long healthy retirement years past their life expectancy, or if the client passes away early into the plan.

So powerful that it helps check all the boxes:

Retire Comfortably ✔️

Strategic and Tax-Efficient ✔️

A little left for the kids ✔️

Flexible if things don’t go according to plan ✔️

As always, the results summarized in this blog post are based on multiple assumptions. Assumptions on taxes, growth rates, illustrated rates, etc, etc. I recommend two follow-up actions:

-

Watch this webinar. It takes this example and goes into the details of everything I discuss here. It takes that 20,000-foot view down to sea level. And, it also goes into the blueprint of the plan with the use of Stonewood Financial reports throughout the process.

-

Give it a try on a client. Reach out to our member success team. They’ll help you identify one client over the age of 60 who agrees with your belief that taxes will be higher in the future than they are today. And give the conversation a shot. You’ll enjoy your client's reaction to what you can do for them.

When it comes to taxes in retirement, there really are approaches that can help 1 + 1 = 3 for your clients. And that is math we can all get excited about.