If you’ve been following our blog this year, you’ve noticed I’ve been sharing some of my favorite message frames.

Message frames are quick, targeted frameworks for communicating a complex topic. And they are incredibly useful in marketing for financial advisors. They can be used in multitudes of ways, from client conversations to seminar content and radio ads.

So to close out the year, I want to share one of the most effective message frames I’ve ever developed: Mandatory vs. Optional.

Let’s set it up.

You’re meeting with a client or prospect who has saved diligently in a 401(k) or IRA. They know, in theory, they have a tax bill coming due in retirement. And perhaps they have considered a Roth or other tax-free conversion to help reduce this tax bill, but just haven’t taken action yet.

How do you get them over the hump?

That’s where the Mandatory vs. Optional framework comes into play.

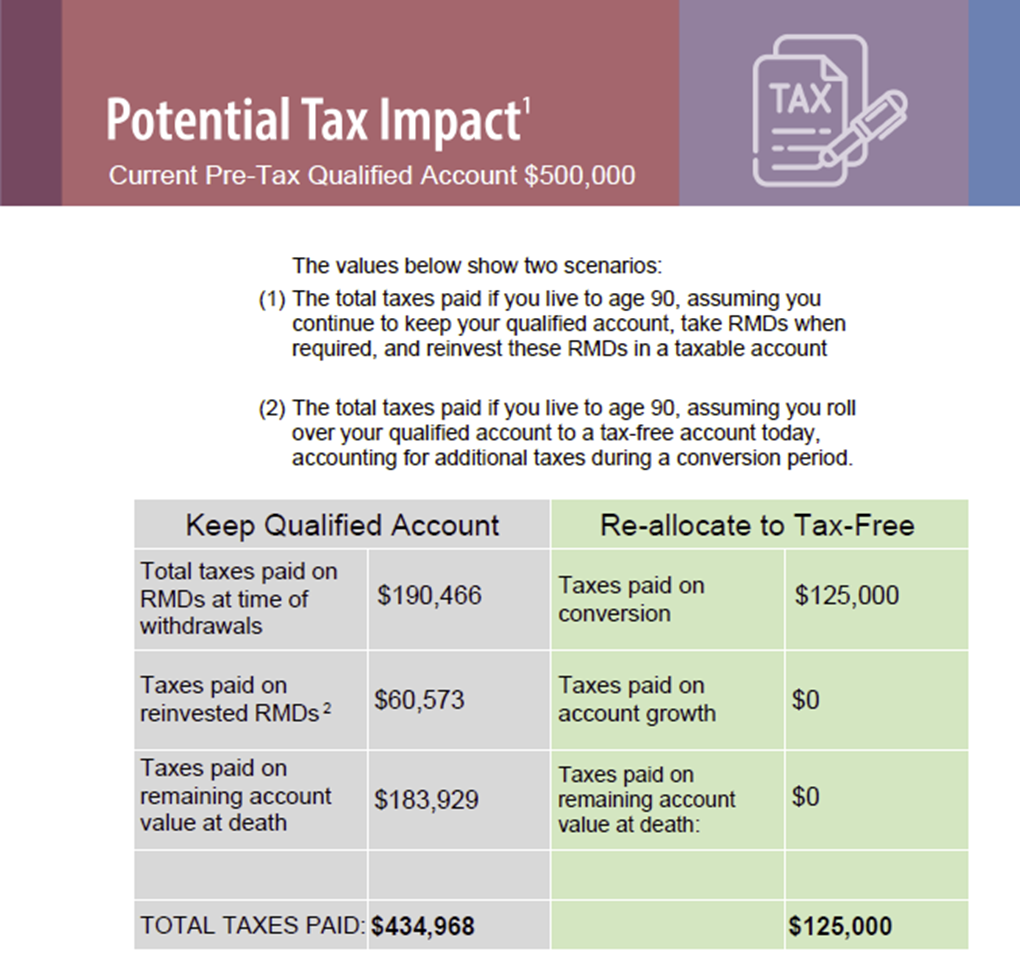

Let’s say you’ve done a Roth analysis for your client. For this blog post, I’ll use Stonewood Financial’s most popular client report, our Total Tax Burden.

This analysis shows the potential amount of taxes a saver will pay if they keep their IRA or 401(k), and the potential amount of taxes they will pay if they convert it to a Roth.

It’s a powerful report. But I’ve found you can drive decision-making behavior even higher by coupling it with this message frame.

Here’s a recent report run on a 60-year-old client.

Once I’ve talked through the analysis, I look at the client and say:

There’s something I notice in your analysis. According to this report, your mandatory, minimum tax bill due to the IRS for this IRA is $125,000. (I motion to the right-hand column.) Essentially, if we paid the taxes you owe today, that tax bill is $125,000.

Unfortunately, there’s not much I can do to reduce this mandatory minimum tax bill. That tax bill has been built up over time based on the way you’ve saved in the past.

However, looking at this report, I see we’re projecting you could potentially pay $434,000 in taxes if you stay on the path you’re on. (I motion to the left-hand column). If I deduce your mandatory taxes from this number, I see that there’s more than $300,000 in optional taxes that you’re choosing to pay - not based on how you’ve saved in the past, but based on how you save from today going forward.

Would it make sense for us to look at some strategies to reduce or eliminate those optional taxes?

This framework is so effective for two reasons:

First, language. Nobody wants to pay optional taxes. We have reframed the difference between their current strategy and a conversion strategy using concepts that empower the saver; we’ve let them know there is something they can do proactively to reduce their optional taxes.

Second, decision-driving. As I talk to advisors, almost all of them have lost a potential client - not to another advisor or strategy, but to inaction. The truth is, even if our clients understand the risks, they are sometimes hesitant to take action. It’s simply easier to keep doing what you’re doing than to make a change. With the mandatory vs. optional framework, we’re helping our clients quantify the cost of inaction.

Sometimes, I’ll frame it up like this:

“Mr. and Mrs. Prospect, when you leave my office today, you’ll have made a choice. It will either be a choice of action to convert a portion of your retirement assets to tax-free and limit your tax bill to the minimum, mandatory taxes. Or it will be a choice of inaction, where you choose to pay more than $300,000 in optional taxes. But it’s a choice either way. I know it can be daunting to make decisions about your retirement nest egg, which is why I wanted to make sure you could quantify the potential tax bill for both paths forward.”

Heads up: Stonewood Financial is rolling out brand-new Roth Conversion software in Q1 that will help you minimize both taxes and IRMAA during your client's conversion - so stay tuned for more on this awesome tool.

So there you have it: our final message frame for 2024. Give it a try, and let me know the kind of response you experience.

As we head into 2025, I’d love to hear your favorite message frames for taxes in retirement, too - connect with me here.