When you and your clients think about annuities, what comes to mind?

Guaranteed income?

Income you can’t outlive?

Security?

An alternative for fixed income?

These are usually the concepts that come to mind.

But what about: Generates Alpha?

While that one might be new to your clients, it’s absolutely true. And it’s a key way annuities will be positioned today and in the years to come.

Annuities have become a staple in the financial planning industry because of the annuities’ ability to provide guaranteed income. Savers have flocked to annuities over the last few decades because of their unique ability to provide a predictable, secure, and even guaranteed stream of income in retirement. That’s made them a critical part of retirement planning since IRAs and 401(k)s on their own offer little protection against these risks.

The annuity market has matured over the past few decades, as annuities have evolved from a niche product to a core base of retirement planning.

Today, we are standing at the precipice of the next evolution of annuities. This evolution isn’t so much based on product design as it is on product positioning.

In today’s market, annuities no longer just deliver income guarantees or security to a portfolio. They help drive Alpha, too.

Alpha is not a word traditionally associated with annuities. It is more of a financial quant’s type of word. It is used to measure the excess return a financial instrument can generate over a benchmark index.

So why bring up that term for an instrument like an annuity that is meant to provide protection? It is not really the goal of an annuity to provide alpha. The goal is to provide safety and guaranteed income. To help clients sleep at night when it comes to their retirement income.

But in many cases, annuities are also driving Alpha in your client’s retirement approach.

Here’s a quick exercise to prove this point. Let’s ask ourselves:

What type of returns would a managed account have to provide to meet the guaranteed income provided by an annuity?

Here’s how we can go about answering this question.

Step 1: Run an annuity illustration, and see what type of guaranteed income an FIA could provide from a defined amount of retirement assets

Step 2: Make some assumptions on what returns you could expect from a managed account with the same amount of money

Step 3: Make some assumptions on how long the client will live

Step 4: Project the amount of income you could take from that managed account over their lifetime

Step 5: Compare the results of the annuity illustration to the results of the managed account projections

I’ve done this. In fact, Stonewood has created software that can do this for every client you have. And the results are quite shocking.

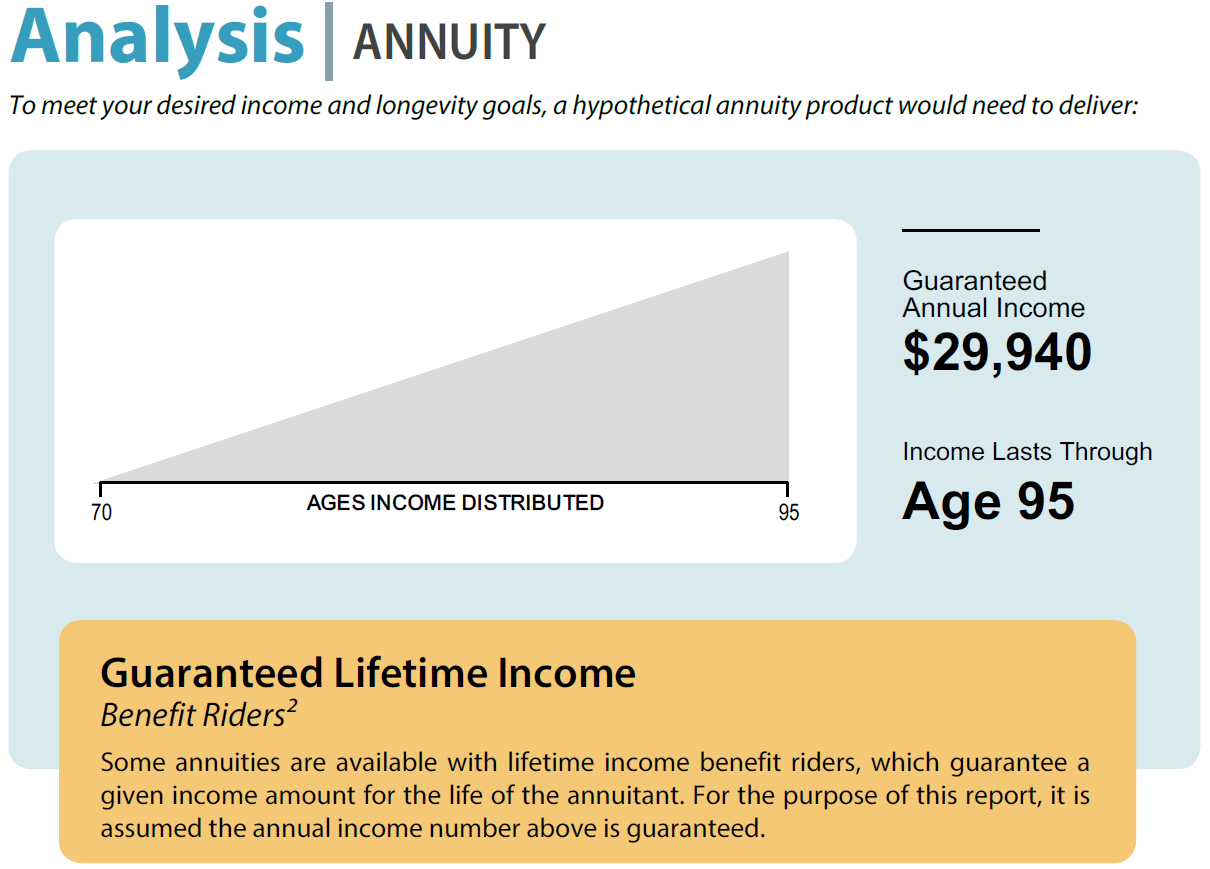

Step 1 - Annuity RESULTS: I ran an illustration from one of the leading carriers that provides guaranteed income. This carrier is one you would think of when looking for a product with one of the higher guaranteed amounts. Less focus on the upside, and more focus on the guaranteed lifetime income amount. As you’ll see in the chart below, for a 65-year-old allocating $200,000 to the annuity, they could guarantee over $29,000 per year for the rest of their life starting at age 70.

Step 2 – Managed Account Assumptions: I have an entire White Paper on setting realistic, reasonable assumptions when comparing a brokerage account or managed portfolio that needs to mitigate market risk through allocation. So, I’ll spare you the soapbox discussion here. Let’s just assume a blended portfolio of 50/50, with a 7.03% growth rate for equities, and a 3.25% growth rate for fixed income. That’s a blended rate of 5.14%. I also assumed a moderate advisory fee of 1.5%. In many cases, when adding up the fee the advisor collects, plus a fee for the third-party asset manager and the cost of the underlying financial instruments in the managed portfolio, that all-in fee is well over 2%.

The 7.03% growth rate for equities represents the average growth rate of the S&P 500 since the turn of the century. And 3.25% represents the average yield of the 10-Year Treasury during the same time frame.

Step 3 – Life span assumptions: How long should we be modeling an income plan for our clients? Should we just be considering Life Expectancy? Math tells me only half of the population makes it to Life Expectancy. So less? I believe that the main job of a financial professional, when dealing with their life savings, is to fund life. Life without income to support that life is a failure. Money needs to be available as long as your clients are alive. This means income planning must extend long beyond life expectancy.

If planning for life expectancy represents half of the population, that tells me that half of those income plans will fail. We can’t have that. No one would settle for that. So, what that means is we need to look beyond Life Expectancy into what we like to call Life Span. For a 60-year-old couple, life expectancy for each is 85. There is a 47% chance one spouse will live to 90. And a 31% chance one will make it to 95. The actuaries will tell you that looking closer at the average financial professional’s book of business; your clients live even longer than these statistics. So, for me, for the portion of the portfolio dedicated to income, the portion of the portfolio funding life, I will always choose to go beyond life expectancy in my projections. For this example, I’ll look at results for plans to age 85, to age 90, and to age 95.

Step 4 – Income comparison: I’m going to look at three different layers of comparison.

First with a focus on matching the annuity’s guaranteed Income Amount. I’m going to calculate how long the income stream from a managed portfolio with the input assumptions would last based on the income amount the annuity is guaranteeing. Basically, a calculation to see how long a systematic withdrawal plan (SWIP) would last.

For the second layer of analysis, I will shift the focus to Longevity. We can certainly model the managed account income projections differently, taking less income from that portfolio to match our lifespan expectations.

The final layer of analysis answers the question…” What would the capital markets have to deliver to match what the annuity guarantees?”

Here are your results:

First the annuity. The best part of the annuity is that the income amount is guaranteed. For life. So for this particular carrier, this 60-year-old example client with $200,000, the guaranteed income at age 70 would be $29,940. Regardless of what the equity markets do. Regardless of what interest rates do. Regardless of how long this sample client lives. $29,940 in the mailbox every year.

Now the income projections from a managed portfolio with the assumptions we provided. 50/50 portfolio, 5.14% blended rate, 1.5% advisory fee. Remember, these assumptions are based on real historical returns since the turn of the century.

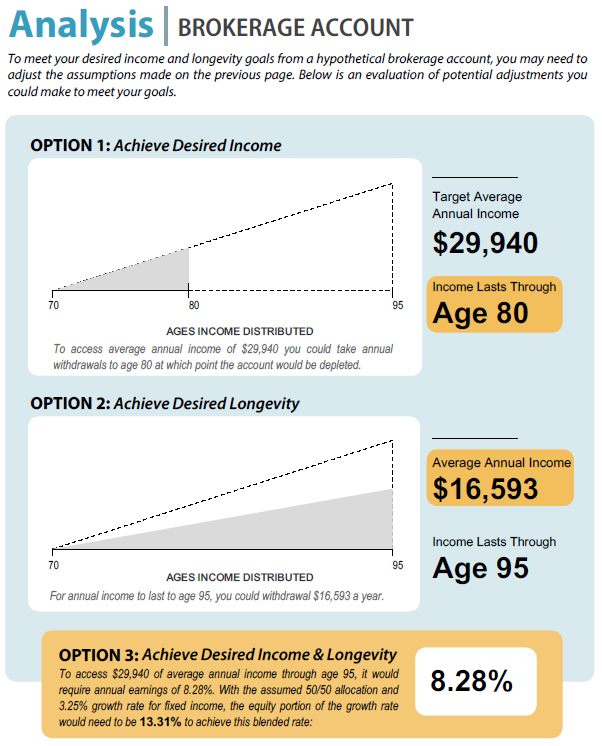

This managed portfolio, trying to match the $29,940 systematic withdrawal that the annuity guarantees, would be out of money by age 80. That’s right. Based on the historical returns detailed above, the managed portfolio would be out of money well short of life expectancy.

In fact, a 23% pay cut would be required to make that distribution last to age 85. To be exact, the client would have to take $23,055 per year to make their managed portfolio last to age 85.

And now for the answer to that question everyone asks… “What would the capital markets have to deliver to match what the annuity guarantees?”. In this case, what would the returns have to be to model at $29,940 distribution to age 85? The answer: 6.78%.

At first glance, you might be thinking, “Well, that’s doable”. And sure, it’s doable. In fact, for many years, results are far higher than 6.78%. Why the problem? This is a BLENDED rate. It’s a blended rate because in a managed portfolio, an advisor must mitigate the client’s market risk through allocation. So to achieve a blended rate of 6.78% in a 50/50 portfolio with the fixed income markets providing 3.25%, the equity portion of the portfolio has some heavy lifting to do. Heavy lifting to the tune of 10.31%. Every year. Now we’re starting to see why the blended rate projections we provided are falling short.

But wait. This is just to make it to life expectancy. And half of those plans fail. What happens when we push the managed account even more? Remember, the annuity is guaranteed. For life. So it’s going to be there regardless of how long the client lives. But the managed portfolio is going to have to work even harder.

See for yourself.

If we push the longevity assumptions to age 90, the annuity looks even stronger.

The managed portfolio would have to deliver a blended rate of 7.74%. Meaning equities would have to provide a 12.23% return. I don’t care who you talk to. No one is projecting north of 12% returns every year from the equity markets.

Push the longevity to 95 and things just look worse for the managed portfolio.

The managed portfolio would have to deliver an 8.28% return. And equities would have to hit a whopping 13.31% average annual return.

These results were shocking to me, even as someone who has been in the annuity industry since the mid-90s.

If this kind of analysis would be helpful to your clients, I’d encourage you to check out Stonewood’s Annuity Alpha software. See how it works, and request a complimentary analysis for a client of your choice. I promise - this software will help you position annuities in a new way, overcome objections, and better serve your client’s income needs.

With all this talk of “Fiduciary Responsibility” in our industry, allow me to ask one final question. If you are an advisor with a fiduciary responsibility, how can you ignore the financial power of an annuity? I’m not suggesting a blanket “every client gets an annuity”. But I do suggest that anyone wearing their fiduciary responsibility as a badge of honor, that you at least give a guaranteed income annuity a look for a portion of some client’s retirement plans.

And with it, you will see the financial power it can provide…

Guaranteed income

For life

With safety

And security

A fixed-income alternative

And now, based on the Annuity Alpha analysis:

Alpha

.png)