Pop Quiz: What’s a big risk of retirement that doesn’t matter much while you’re saving… but can matter a LOT once you’re retired?

If you answered “Sequence of Returns Risk,” you’re right.

Sequence of Returns Risk is one of those risks that most savers have never considered as they enter retirement. And it’s easy to see why: It’s a risk that just doesn’t have an impact during someone’s saving years.

However, it’s a risk that can rear its ugly head in retirement, so it’s important that American savers understand the risk, its potential impact, and how to protect against it. With all the market volatility we’ve witnessed this month, it’s a good time to take a closer look at this risk and how we can help clients prepare.

What is Sequence of Returns Risk?

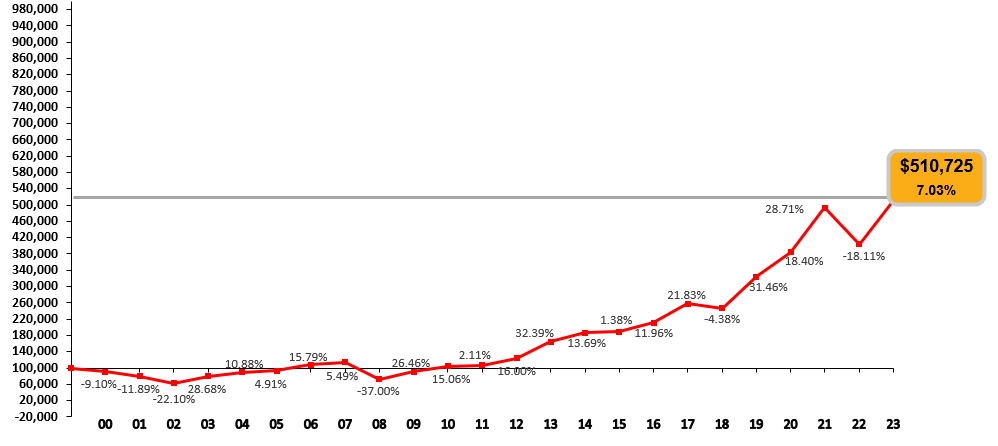

Sequence of returns is the name given to the pattern of returns an account, index, or market experiences. If we’re looking at the S&P 500®, for example, there is a pattern of returns that has occurred over the past few years: In 2021, the market was up 28%. In 2022, it was down 18%. In 2023, it was up 26%.

For most savers, the sequence in which their returns come in doesn't matter much while they’re saving. Here’s a quick example to show you why.

Let’s say a saver has $100,000 in an IRA growing at the rate of the S&P 500®. In real life, here’s the growth those funds would have seen so far this century:

At the end of last year, the $100,000 would have grown to $510,000, despite some ups and downs in the index.

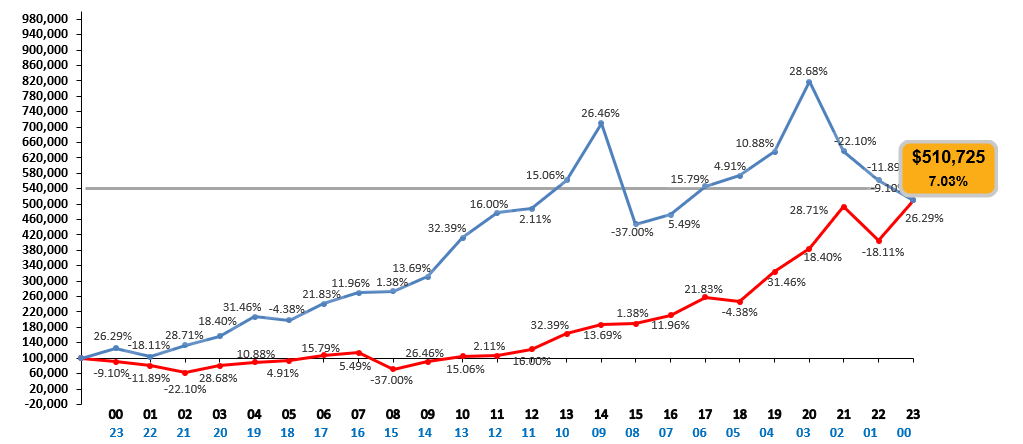

But now let’s see what would happen if the S&P 500® experienced those returns in reverse.

To be clear: We’re not changing the returns. We’re just projecting what would happen if those returns happened in the opposite order: If 2000’s return happened in 2023, and 2001’s return happened in 2022, etc.

The blue line is the result if we had experienced this decade’s returns in reverse:

As you can see, the pattern is very different, but the funds in the account end up in the exact same place - having grown to about $510,000.

This is why most savers have not considered Sequence of Returns Risk in their retirement approach: while all the money in your account is rising and falling with the returns, it doesn't matter what order those returns come in.

So Where’s the Risk?

Of course, a big shift happens when a saver retires.

Suddenly, they are withdrawing money from the account each year to use as income. And that’s when Sequence of Returns Risk can rear its ugly head.

The “Risk” comes when you need to access your funds, because suddenly you don’t have all of your money recovering from market losses. In retirement, savers often need to withdraw money for living expenses regardless of whether the market is up or down - which means that in a down market, they are withdrawing funds at a potential loss.

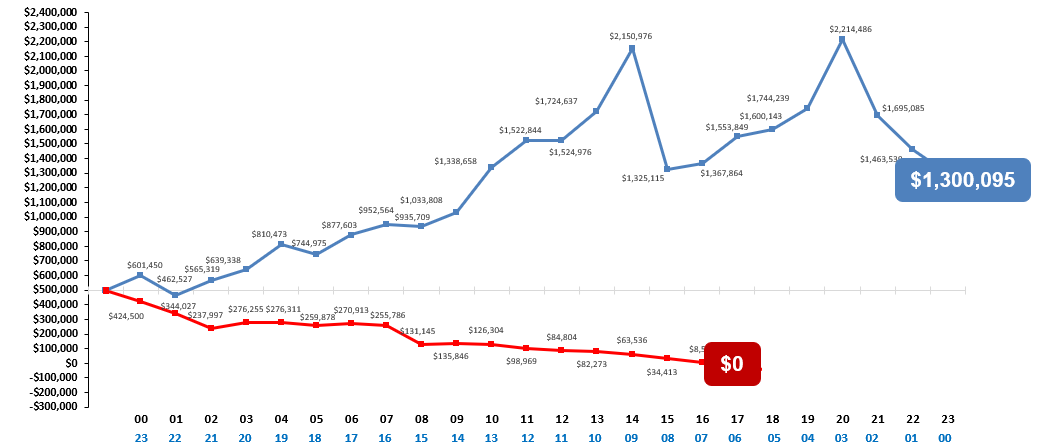

So let’s run our example again, but this time assume the saver is retired and needs to access retirement income from the account. Let’s say this saver has a $500,000 IRA growing at the rate of the S&P 500®. She retires in 2000 and takes $30,000 a year out of the account for income.

In real life, this is what would have happened:

That’s right: She runs out of money in 2017.

Unfortunately, she had to withdraw money in 2000, 2001, and 2002 (not to mention 2008) - all while the market was down and there were fewer funds in her account. That means she has less money available to participate in the market’s recovery in the following years.

Now let’s look at what would happen if we reversed the sequence of those returns. Again, we’re not changing the returns of the market; we’re just projecting what would happen if those returns happened in reverse, with the 2000's return coming in 2023 and so on.

If we experienced this decade in reverse, here are the results:

Not only does this saver not run out of money, she actually has over $1 million left at the end of this period.

Now you can see that Sequence of Returns Risk doesn’t matter much to your clients while they’re saving for retirement - but it can become a big headache for them in retirement.

How You Can Help

There’s no shortage of advice on helping your clients address Sequence of Returns Risk.

But one strategy you might not know about is leveraging certain product designs to address this risk.

We’ve talked in this blog before about leveraging Index Universal Life insurance in the retirement income space. But the product design of IUL can also help savers address sequence of returns risk. This is thanks to the interplay of both indexing and participating loans available in many IUL products, features that allow interest credits to both funds in the cash value of the policy and funds borrowed through policy loans to use as supplemental retirement income.

Regardless of how you plan to address Sequence of Returns Risk for your clients, it’s a risk they need to understand.

We’ll see if the rest of 2024 is as rocky as the past few weeks have been. But one thing is for certain: Over your client’s lifetime, there will be up-market years and down-market years. While we can’t control the market or the pattern of those returns, we can help protect their assets from the impact of these changes.

Looking for a powerful way to explain Sequence of Returns Risk to your clients and prospects? Stonewood Financial has a suite of market tools - from seminar presentations to client handouts - that can help. Check them out here.

.png)