Advisors who help their clients mitigate tax and legislative risk in retirement naturally spend a lot of time helping clients convert qualified funds into tax-free vehicles.

If you’re one of those advisors or want to become one, you’ll undoubtedly start to hear the question, “How much of my IRA should I convert this year?” Or perhaps, “How much of my IRA should I convert over the next few years?”

To truly mitigate the risk of rising taxes, it’s not enough to simply optimize the kinds of retirement vehicles your client is using. You also have to optimize the way they convert funds into those vehicles.

However, the answers to these questions can vary wildly depending on multiple variables.

Let’s dive deep into the question - and how you can help answer it for your clients.

Evaluating Tax-Free Conversions

First off, the most important question: Should you and your client be considering a conversion?

Where do you and your client think taxes are headed? Clearly, if you and/or your client think taxes are going to be the same or lower in the future, then conversion could be off the table.

But perhaps the question should be asked slightly differently. Do you and/or your client believe taxes COULD be higher in the future than they are today?

COULD - representing risk - is an important word.

Looking at history, “the market” is usually up. In general, I believe the market will go up over the long run. But it COULD go down, so that means I need to diversify my portfolio to protect against the chance that it does.

As fiduciaries, we need to understand the importance of COULD. And if taxes COULD go up, our clients SHOULD be diversifying the taxation of their retirement assets.

Once you and your client have established that a conversion plan is necessary, you now need to explore how quickly to convert those assets. And with that, you introduce a few variables that must be considered.

Considerations in a Conversion

Here are the variables you’ll want to analyze for your clients:

- Tax Drift – with a progressive taxation system, converting assets in a given year could push your client into a higher tax bracket during the conversion years. We call this “Tax Drift”. (Stonewood Financial actually has software to evaluate this for your clients, you can check it out here.)

- Potential Changes to Future Tax Rates – if you have a multi-year conversion plan, taxes can (and likely will) change during that plan. Congress has every right to change the rules on retirement assets. (If you want to dive a little deeper into the ways Congress can make changes, you can download a white paper by my colleague here.)

- IRMAA – the “Income-Related Monthly Adjustment Amount” is an additional premium paid on top of Medicare Part B and D premiums based on income. In other words, a tax on your Medicare Part B and D insurance is based on how much money you make. Converting IRA assets to tax-free in a given year will increase your income levels, potentially increasing your IRMAA.

One important number NOT on the list?

The amount of income tax paid within your client’s existing tax bracket.

The Difference Between Your Client's Tax Bill and Tax Drift

We should consider IRA conversions in a self-contained manner. I always assume that every IRA dollar is eventually going to get taxed. Therefore, the crucial value of an IRA should always be the after-tax value. The amount going to the IRS from an IRA is not your client’s money. It will always belong to the IRS. So the question is not if the money is going to the IRS; it’s when.

You don’t create a Retirement Tax Bill by converting - you simply expose it. Money will definitely shift sides of the balance sheet. But if you are looking at the IRA value as an after-tax value, then the value of the IRA is the same both before and after the conversion. You just let the IRS have the money that was already theirs.

Tax drift is different. If the conversion pushes your client into a higher bracket, then the portion in the higher bracket is important. That is money your client would not have to pay if there was no conversion. And that is why Tax Drift will be a big part of the following example.

Optimizing Your Client's Tax-Free Conversion

Let’s get started.

First, some assumptions.

Let’s examine four hypothetical couples and how changes to the variables above could impact them.

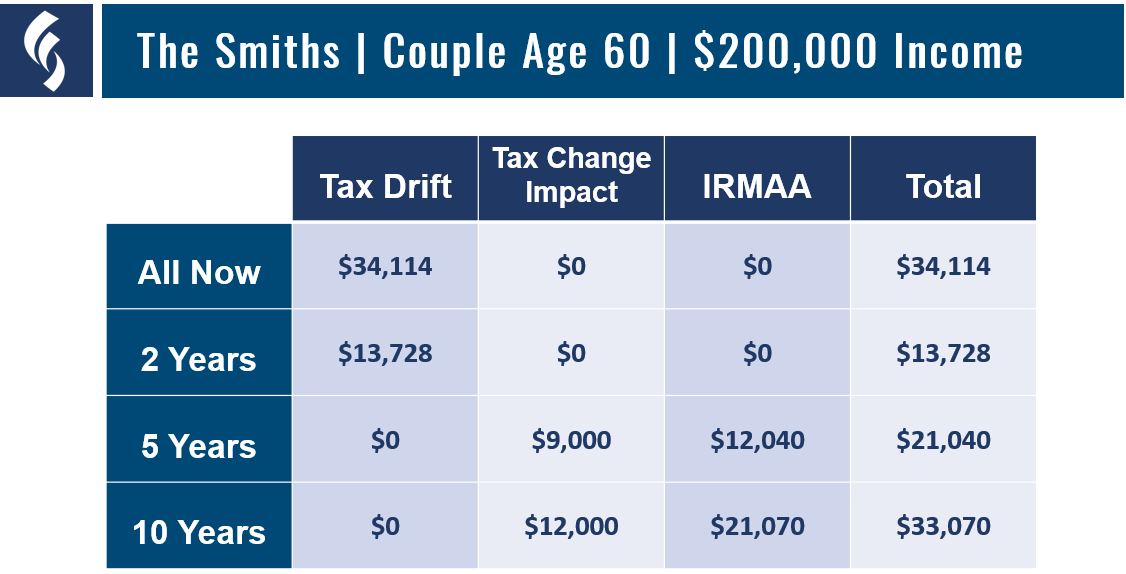

Couple 1 – “The Smiths” Age 60, with $200,000 of Adjusted Gross Income (AGI) before the conversion

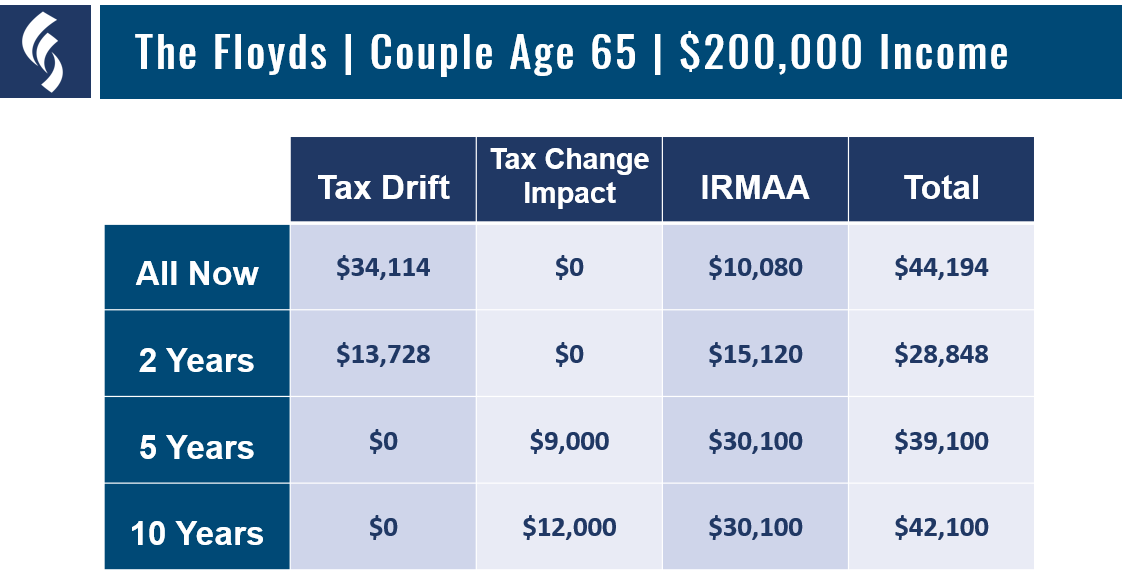

Couple 2 – “The Floyds” Age 65, with $200,000 of Adjusted Gross Income (AGI) before the conversion

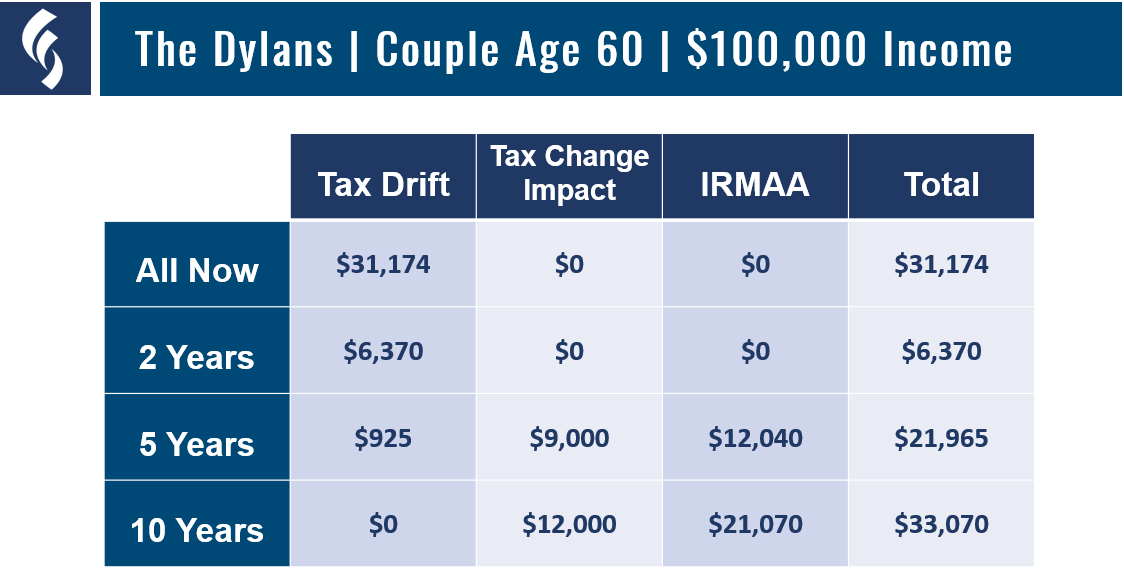

Couple 3 – “The Dylans” Age 60, with $100,000 of Adjusted Gross Income (AGI) before the conversion

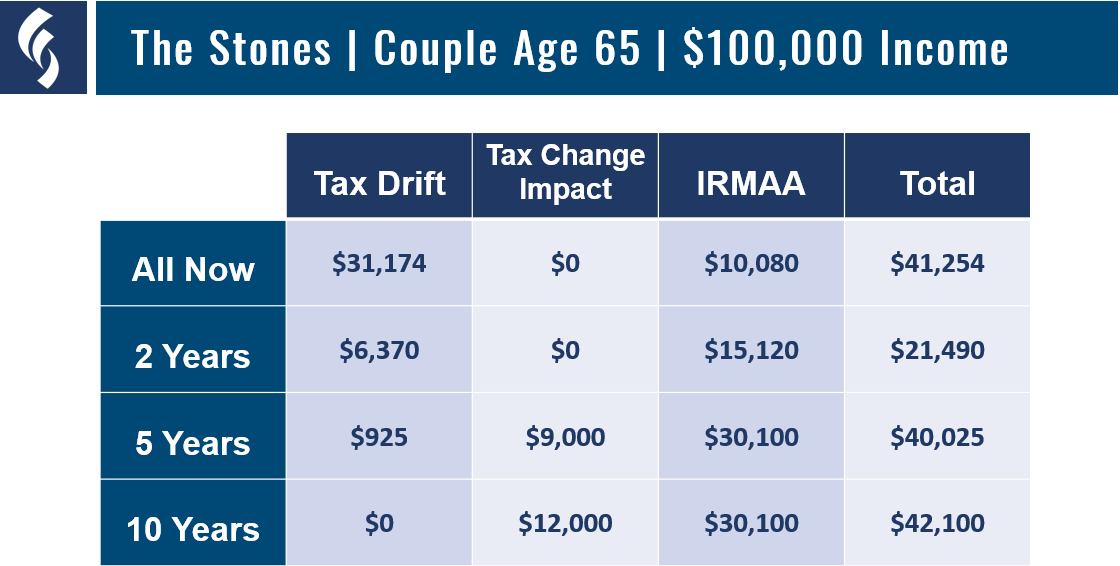

Couple 4 – “The Stones” Age 65, with $100,000 of Adjusted Gross Income (AGI) before the conversion

All four couples are looking to convert $500,000 of their IRA dollars into a Roth IRA. You’ll see from the assumptions that I’m varying the age of the couple and their AGI. These two variables impact Tax Drift and IRMAA calculations.

Using IRMAA tables, the general impact of conversion is about $1260 a year, per tier, per person, for Medicare Part B; and another $245 a year, per tier, per person, for Part D. So that adds up to be an additional $1505 for every year IRMAA is impacted, for every tier you jump, for both husband and wife.

For each example, I’m going to look at four different conversion patterns:

-

Converting everything in year 1

-

Converting over 2 years

-

Converting over 5 years

-

Converting over 10 years

As a general rule, the more you spread out the conversion, the less tax drift you will have, because you’re adding less income in any given year.

But I’m also going to assume a tax increase in year 3 of all these conversion strategies. This comes from the assumption that the current lower tax bracket rates passed as part of the 2019 Tax Cuts and Jobs Act (TCJA) will sunset in 2025, and brackets will revert to their older, higher rates in 2026. The assumption is an increase of 3% to the couple’s effective tax rate.

Now let’s look at each couple’s options and how the taxes play out in the various situations.

You can see in the tables above the general trend. Converting assets quickly can increase the tax drift while slowing down the conversion can lead to both higher taxes because of looming tax increases and more years subject to additional IRMAA.

Of course, these are general trends. The optimal conversion pattern can vary greatly based on your beliefs, your assumptions, and even the age of the client considering conversion.

As you read the tables and data above, it’s important to make a key distinction. A few benefits of conversion that are not really highlighted in the analysis must still be considered:

- Tax changes – while having to pay some extra dollars during the conversion may seem like a “penalty”, keep in mind these assets will be immune from all future tax hikes. In fact, if taxes increase during the conversion, your IRA dollars will eventually have to pay those higher rates. The question then becomes would you rather pay those only during the conversion, or continue to pay them throughout your lifetime?

- IRMAA – paying additional IRMAA comes off like a penalty in this analysis. However, the benefit of having these dollars off the books from future IRMAA calculations can far outweigh the additional premium paid during the conversion.

In summary, conventional wisdom for our industry may not quite be accurate all the time. Most advisors will recommend to their clients to convert everything up until the next tax bracket. But you can see from the results it may pay off to convert assets a little more quickly. Especially if you believe taxes are on the rise.

Does anyone think taxes are going down? It’s a safe assumption to say no.

Helping Your Clients

If you’d like to dive deeper into optimizing tax-free conversions for your clients, I invite you to watch this recent Stonewood Financial Study Group recording. In it, I detail how to evaluate and optimize conversions for your clients.

And, of course, if you need help, the team at Stonewood Financial is here for you. We can show you our Tax Drift software and answer any questions you might have - just reach out to our team.